This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Insurance technology veteran Sandra DeSilva has announced the launch of Mythen, an artificial intelligence (AI)-powered parametric insurance platform and reinsurer, based in Bermuda and Texas, that specialises in writing natural catastrophe risks.

Mythen, is comprised of a team of global insurance, reinsurance and technology experts who aim to leverage advanced technologies in order to provide liquidity and coverage for otherwise difficult to insure risks.

According to the announcement, Mythen’s multi-disciplinary team of industry veterans will use AI, machine learning, underwriting, modelling, remote sensing, and other technologies for developing insurance products, structuring coverage, and taking risk.

“We are using the latest technologies and working with highly-skilled partner companies to penetrate deeper into the insurance market with products across the natural and other catastrophe risk spectrum,” commented DeSilva.

She continued: “We are motivated to help combat climate change and close the widening insurance gap by providing the technology to administer global portfolios subject to climate risk and uncertainty.

“I am delighted with the team as we are addressing critical social and environmental needs.”

Moreover, Mythen Holdings Bermuda oversees Mythen Insurance Services, and is made up of a Texas-based managing general underwriter (MGU), as well as a claims service unit, Mythen Claims Services, and Mythen Re, which is a Bermuda Class 3a insurer which has a fully collateralized Bermuda segregated cell, Eiger 2025.

The organisation has ambitions to help alternative reinsurance capital sources, including those from the insurance-linked securities (ILS) market, access more risk in parametric form.

Therefore, by offering structured parametric solutions, Mythen seeks to bridge the gap between ILS investors and natural catastrophe risk, which will ultimately help create new opportunities for efficient capital deployment.

In addition, Mythen has also partnered with Texas-based insurer Southlake Specialty Insurance Company, which provides paper, fronting, and leverage, while the MGU enjoys quota share coverage from partners in the wider reinsurance market.

“Mythen’s parametric solution is a prime example of Southlake’s dedication to innovation and the use of technology to drive the insurance industry forward. Sandra’s team is addressing the critical challenge of providing first-dollar coverage in a complex market. After seeing the demo, we immediately recognized its potential to revolutionize how businesses manage wind exposure—and knew we had to be part of it,” said Yogesh Kumar, CEO of Southlake.

At the core of Mythen Insurance Services is a technology platform that links data, risk analytics, and forecasting expertise to manage portfolios and covering insurance risk.

The company has begun underwriting windstorm risk, namely US hurricane risk, utilising parametric trigger products designed to minimise the time time to pay claims as well as keeping internal expenses low.

Engineered for simplicity and accessibility, the product is tailored for brokers and clients, ensuring seamless adoption.

At the same time, Mythen’s WindSpeed™ technology and online platform enables instant quoting, portfolio management, while also allowing for upscaling risk and seamless hedging.

AI-powered parametric platform Mythen launched by DeSilva in Bermuda was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

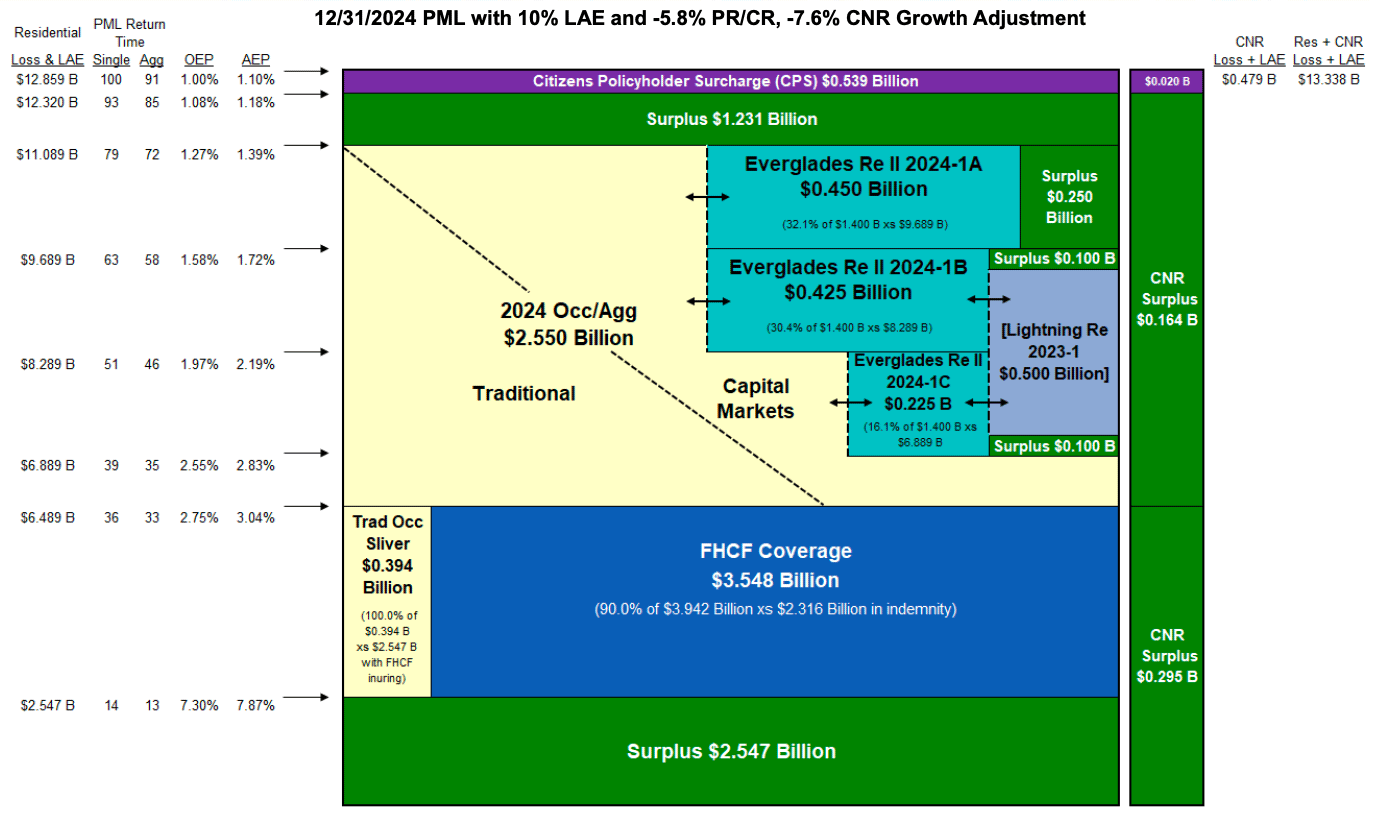

Florida Citizens still has

Florida Citizens still has