This content is copyright to www.artemis.bm and should not appear anywhere else, or an infringement has occurred.

Over the last few years, there has been a significant shift in sentiment among mainstream media and politicians, who cite the cost of reinsurance coverage as a key driver of the escalating cost of property insurance in the United States and nowhere has this been more apparent than in Florida.

The cost of reinsurance has been rising, as reinsurers and third-party capital providers, including ILS fund managers, seek to get paid adequately for the natural catastrophe exposure they are assuming, having been badly impacted by catastrophe and weather losses over repeated years.

Reinsurance has become an easy target for those looking to identify a driver of rising property insurance rates for consumers, especially given how fast and far the market has hardened over the last two years.

As an international financial market dealing in billions of dollars and with offshore centers of expertise, unfortunately reinsurance also fits a narrative for those who would prefer to shift the focus of blame for problems in the US property insurance market offshore, as well.

Which means it has become a contentious issue in political circles, especially in the US states that have been most affected by natural catastrophes and severe weather.

As ever, Florida is one of those states in focus and it seems that not a week goes by without mainstream press citing the cost of reinsurance as one of the issues keeping property insurance prices high for policyholders in the state.

Of course, pinning the blame for high property insurance costs on carriers’ expenditure on reinsurance protection overlooks all of the other drivers, many of which have been issues since long before this hard market came along.

Aside from the losses and the frequency claims that had been passed onto reinsurers, before the sector reset its attachments higher and reduced aggregate coverage, there have also been significant inflationary factors that have driven exposure values sky-high, as well as the excess and amplified cost of claims being driven by litigation and an industry that burgeoned with a focus on working to inflate the quantum of property claims.

None of this is unique to Florida either. It’s just a lot of this became more accentuated as it was professionalised there, while litigation and fraudulent claims have been something quite unique to behold in the Sunshine State.

Property insurance rates were bemoaned as problematic and too high in Florida well before 2017, at which time the reinsurance market was incredibly soft compared to the state of the market today.

The situation in Florida is also accentuated by the fact some of the domestic market insurance carriers have historically been relatively thinly capitalised, compared to nationwide players and so rising reinsurance costs have hurt them much more, while rising attachments have also proven problematic to their business models.

Which drove the state’s legislative to introduce more state-backed reinsurance support, which elevated the issue much higher and drove greater media awareness as well.

So, reinsurance as a topic, has been making its way up the political and media agenda and in the last year hit the state Governor’s budget, as Ron DeSantis set funds aside to pay for a study into reinsurance market cycles.

Earlier this year, Governor Ron DeSantis signed his budget for fiscal year 2024-2025, dubbed ‘Focus on Florida’s Future’.

There are a raft of insurance and risk mitigation measures within the budget, with some $237 million set aside for budget support of residential home mitigation programs and additional oversight of the property insurance market in Florida.

Within that, a small line item allocates $475,000 for contracting reinsurance industry experts to evaluate the impact of reinsurance cycles on property insurance rates.

There is no line item, that we can see, designed to pay for analysis of other factors driving property insurance rates in the state.

The property insurance market in Florida has been stabilising, with the effects of legislative reforms undertaken in recent years clearly one reason for this. While carriers capital positions have also improved, helped by a lower level of catastrophe and attritional losses last year.

This is also helping to improve conditions for buying reinsurance for carriers in the state, as seen at recent renewals.

But the fact remains, it is unfair to blame reinsurance markets for Florida’s high property insurance prices, or indeed for any other US state.

That has much more to do with the levels of exposure, inflation, values-at-risk, losses and all the aforementioned challenges with litigation, claims amplification and even outright fraud that has been seen after major losses struck the state.

We must not forget the fact Florida is ground-zero for exposure values to hurricane risk and while building codes and practices have improved, it remains true that any medium to major hurricane hitting the state can cause billions of dollars in losses for insurers and reinsurers.

At which point the reinsurance market always demonstrates its worth, as without it Florida’s insurance market would surely need to be fully-subsidised by the state government and its taxpayers.

Understanding the effect of reinsurance cycles on the rates property insurers charge in Florida is, of course, worth some effort.

Reinsurance rates go up. So too property insurance rates are likely to rise. But this has nothing to do with the true cost of doing business there, given the rapidly rising exposure and increasing values of property in the way of hurricanes, or other natural events.

The state might do better to analyse the effects of Florida specific idiosyncrasies, in the legal, adjusting, construction and repair marketplaces, as well as how those drove insurance rates higher over the last two decades.

While another worthwhile venture might be in exploring ways to buy reinsurance more efficiently, or how innovative risk transfer such as parametric triggers might be able to play a role and create different, perhaps better, economics for carriers in their interactions with reinsurers.

But understanding reinsurance market cycles and the influence they have on primary insurance rates may not lead to the kinds of learnings that can make much of a difference in the first place.

Supply and demand side factors, such as capital availability and risk appetite, are often driven by global factors, as well as local. Alongside which, there is a need for risk commensurate rates to be paid for both insurance and reinsurance. Subsidising that is not an industry concern, but the industry can provide solutions that might help add efficiency through pooling of risk and leverage of efficient sources of risk capital.

This market has itself been trying to understand reinsurance cycles for decades and in recent history many extremely well-qualified participants thought the reinsurance cycle was dead. That proved not to be the case, at least not in the way anyone thought.

The reinsurance cycle is alive and kicking and we’ve been trying to second-guess it for years.

We wish DeSantis and his team luck and hope they’ll share the findings from their chosen consultants.

I’m sure many reinsurers and ILS funds that deploy billions in capital to support Florida’s property insurance marketplace and the state’s inhabitants would welcome that too.

Florida Governor DeSantis wants to understand reinsurance cycles was published by: www.Artemis.bm

Our catastrophe bond deal directory

Sign up for our free weekly email newsletter here.

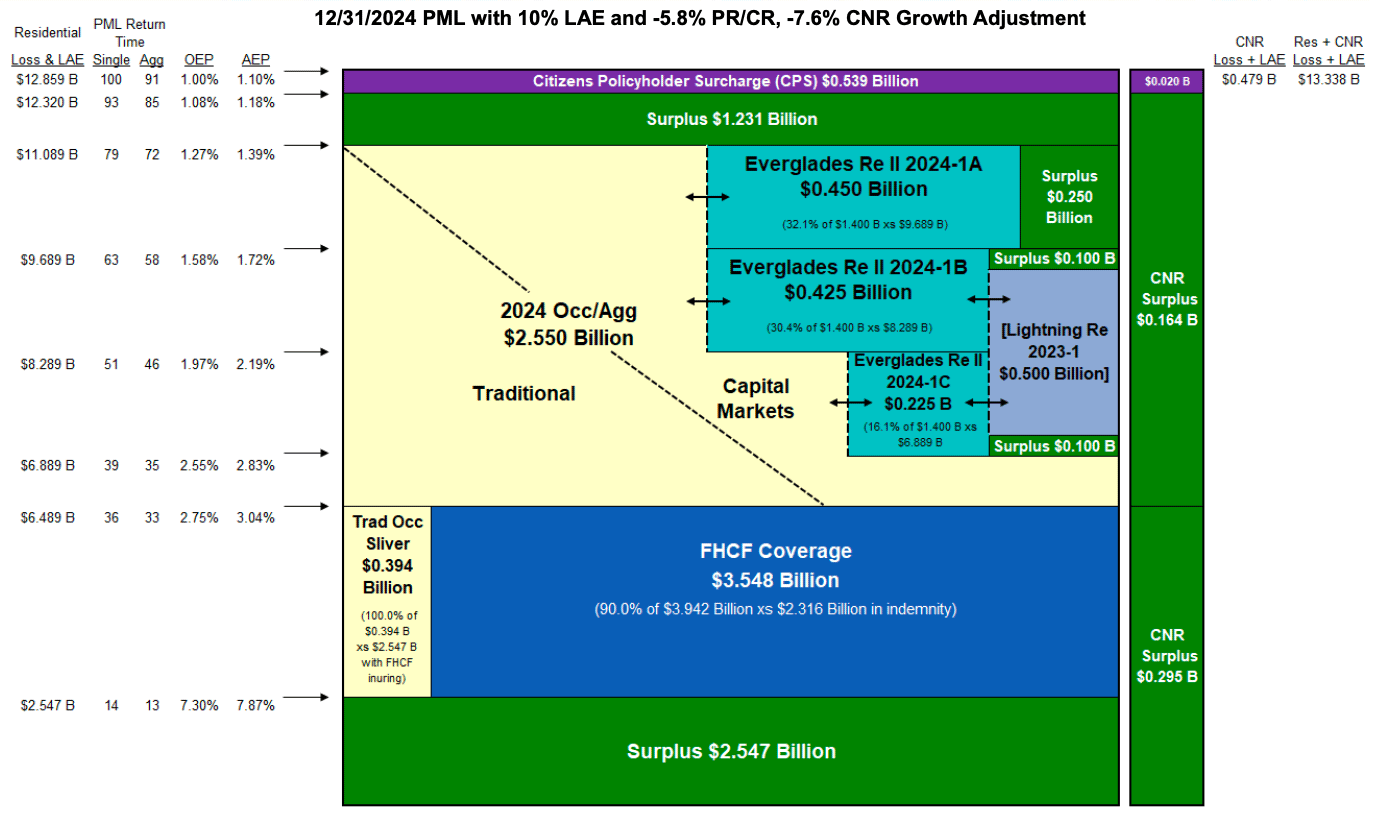

Florida Citizens still has

Florida Citizens still has